Section 11-4: Other Types of Life Insurance

Section 11-4: Other Types of Life Insurance

Overview

In addition to term life insurance, there are several other types of life insurance policies available, each with its own features, benefits, and suitability for different financial goals. Here are some common types of life insurance:

In addition to term life insurance, there are several other types of life insurance policies available, each with its own features, benefits, and suitability for different financial goals. Here are some common types of life insurance:

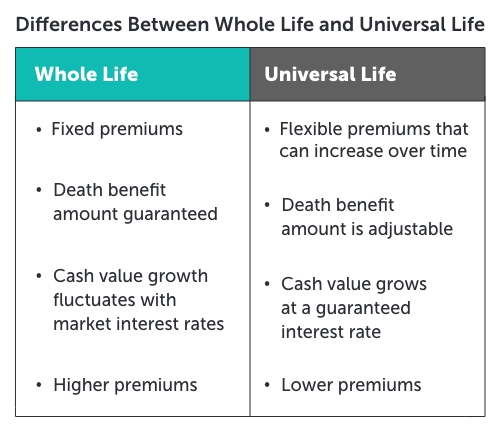

Whole Life Insurance: Whole life insurance provides coverage for your entire life, as long as premiums are paid. It also includes a cash value component that grows over time, with a guaranteed minimum interest rate. Policyholders can access the cash value through loans or withdrawals, although this may reduce the death benefit. Premiums are typically higher than term life insurance but remain level for the life of the policy.

Universal Life Insurance: Universal life insurance offers more flexibility than whole life insurance. Policyholders can adjust the premium payments and death benefit amount over time, subject to certain limits and guidelines. Like whole life insurance, universal life insurance includes a cash value component that earns interest at a variable or guaranteed rate. Universal life insurance policies may also offer the option to skip premium payments if there is enough cash value to cover the costs.

Variable Life Insurance: Variable life insurance allows policyholders to allocate the cash value portion of the policy to investment sub-accounts, similar to mutual funds. The cash value and death benefit can fluctuate based on the performance of the underlying investments. Variable life insurance offers the potential for higher returns but also comes with greater investment risk. Policyholders may need to pay additional fees and charges associated with managing the investment component of the policy.

Indexed Universal Life Insurance: Indexed universal life insurance combines features of universal life insurance with the potential for higher returns linked to the performance of a stock market index, such as the S&P 500. Policyholders can participate in market gains up to a certain cap while being protected from market losses. Indexed universal life insurance offers a balance of flexibility and growth potential, making it popular among individuals seeking both insurance protection and investment growth.

Final Expense Insurance: Final expense insurance, also known as burial insurance or funeral insurance, is a type of whole life insurance designed to cover end-of-life expenses such as funeral and burial costs, medical bills, and outstanding debts. These policies typically have lower death benefits and are easier to qualify for compared to traditional life insurance policies.

Guaranteed Issue Life Insurance: Guaranteed issue life insurance is a type of whole life insurance that is available to applicants without the need for a medical exam or health questionnaire. These policies have guaranteed acceptance as long as the applicant meets the age requirements, typically between 50 and 85 years old. Guaranteed issue life insurance may have higher premiums and lower death benefits compared to other types of life insurance.

Each type of life insurance has its own advantages and considerations, so it's important to carefully evaluate your financial needs, goals, and budget before choosing a policy. Working with a licensed insurance agent or financial advisor can help you determine the most appropriate type and amount of life insurance coverage for your individual circumstances.

Videos (Click on Image to View Videos)

Term vs. Whole Life Insurance

Types of Life Insurance

Online Textbook Read Section 11-4: (Other Types of Life Insurance)