Unit 3: Supply and Demand

Unit 3: Supply and Demand

Unit 3: Supply and Demand

Unit 3: Supply and Demand

Unit 3: Supply and Demand

Supply and demand are fundamental concepts in economics that describe the relationship between the quantity of a good or service that producers are willing to offer for sale (supply) and the quantity that consumers are willing and able to purchase (demand) at various prices.

Demand:

Definition: Demand refers to the quantity of a good or service that consumers are willing and able to buy at different prices during a specific period.

Law of Demand: According to the law of demand, there is an inverse relationship between the price of a good and the quantity demanded, holding other factors constant. When the price of a good decreases, the quantity demanded increases, and vice versa.

Demand Curve: A demand curve is a graphical representation of the relationship between price and quantity demanded. It slopes downward from left to right, indicating the inverse relationship between price and quantity demanded.

Determinants of Demand: Factors that influence demand include:

- Price of the good or service

- Income of consumers

- Prices of related goods (substitutes and complements)

- Tastes and preferences

- Expectations about future prices and income

- Number of buyers in the market

Supply:

Definition: Supply refers to the quantity of a good or service that producers are willing and able to offer for sale at different prices during a specific period.

Definition: Supply refers to the quantity of a good or service that producers are willing and able to offer for sale at different prices during a specific period.Law of Supply: According to the law of supply, there is a direct relationship between the price of a good and the quantity supplied, holding other factors constant. When the price of a good increases, the quantity supplied increases, and vice versa.

Supply Curve: A supply curve is a graphical representation of the relationship between price and quantity supplied. It slopes upward from left to right, indicating the direct relationship between price and quantity supplied.

Determinants of Supply: Factors that influence supply include:

- Price of the good or service

- Cost of production, including labor, materials, and technology

- Prices of inputs (e.g., raw materials, energy)

- Technology and productivity

- Expectations about future prices and costs

- Number of sellers in the market

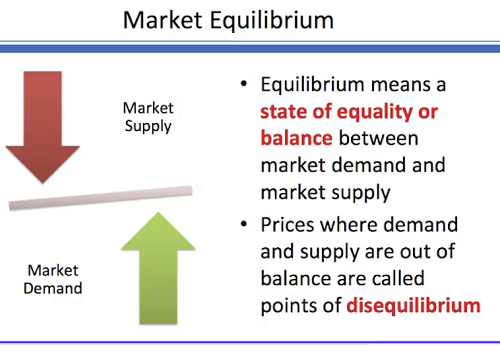

Market Equilibrium:

Market equilibrium occurs when the quantity demanded equals the quantity supplied at a particular price, resulting in no surplus or shortage in the market. The equilibrium price and quantity are determined by the intersection of the supply and demand curves.

Changes in supply or demand can shift the equilibrium price and quantity. For example, an increase in demand will lead to a higher equilibrium price and quantity, while a decrease in supply will lead to a higher price but a lower quantity.

Understanding supply and demand dynamics is essential for analyzing market behavior, pricing decisions, resource allocation, and the functioning of the economy as a whole. It provides insights into how changes in prices, incomes, preferences, and other factors affect consumer and producer behavior and market outcomes.

Vocabulary

Lesson Reading

Videos and Interactives (Click on Images to View Content)

Supply and Demand Video

Supply and Demand